The idea of eliminating the Federal Deposit Insurance Corporation (FDIC) is not only impractical but a serious threat to the financial security of millions of Americans. Established during the Great Depression, the FDIC has played a vital role in maintaining economic stability by insuring deposits and ensuring public confidence in the banking system. Removing this safeguard could lead to catastrophic consequences, including widespread financial panic and systemic instability.

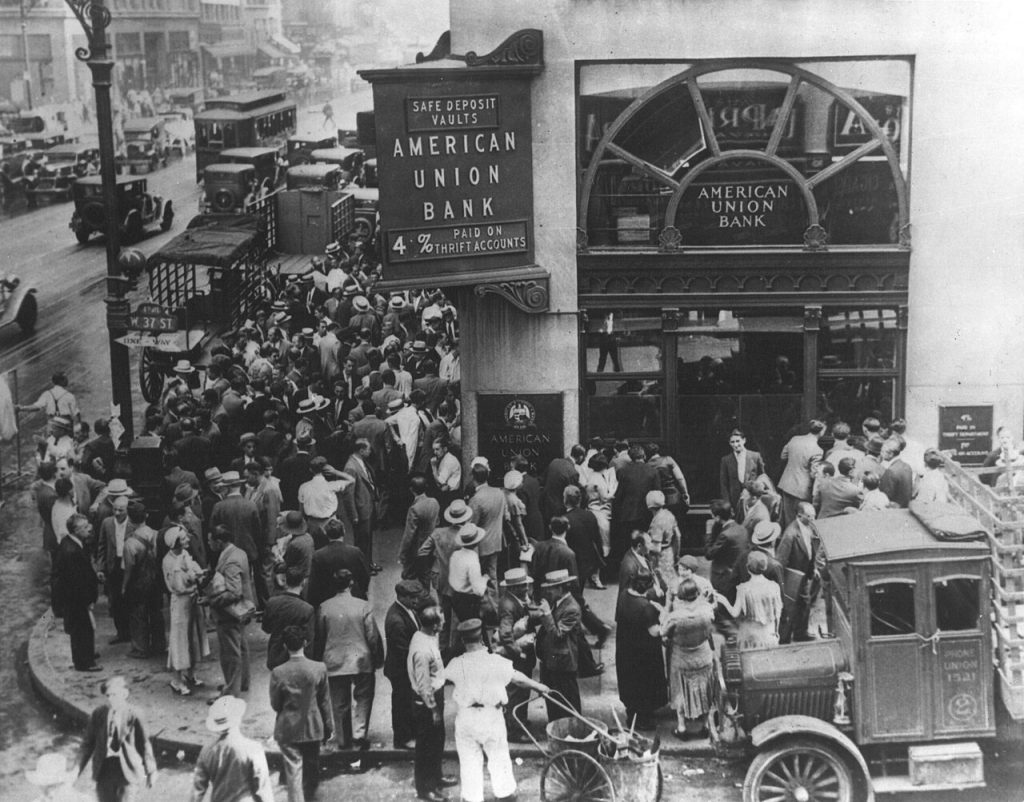

The FDIC provides deposit insurance for accounts up to a certain limit, offering reassurance to depositors that their money is safe even if a bank fails. This confidence is a critical factor in preventing bank runs, where customers withdraw funds en masse due to fear of losing their savings. Historically, such runs have led to widespread economic disruption. Without the FDIC, depositors would have no such guarantee, making the banking system far more vulnerable to sudden, destabilizing withdrawals.

The Banking Act of 1935 was signed by President Roosevelt. Proposals to shift the FDIC’s responsibilities to the Treasury Department show a fundamental misunderstanding of the agency’s role and funding structure. The FDIC is financed by premiums paid by banks, not taxpayers, and operates independently to avoid political interference. The Treasury, as a politically influenced body, lacks both the operational independence and the expertise to manage bank failures or oversee deposit insurance effectively. This change would create inefficiencies and erode the public trust essential to a stable financial system.

The consequences of dismantling the FDIC would likely extend beyond the financial sector, disproportionately impacting working-class families and small businesses. These groups rely heavily on the security of insured deposits to protect their savings and sustain operations during economic downturns. Removing this layer of protection could leave millions vulnerable to financial loss in the event of a banking crisis.

Even the suggestion of eliminating the FDIC could create immediate turmoil in financial markets. Consumers might begin to question the safety of their deposits, leading to precautionary withdrawals and potential liquidity crises for banks. The ripple effects of such uncertainty could destabilize the broader economy, amplifying risks for both individuals and businesses. Much like the self feeding loop that caused the crisis in the 1930’s.

Proponents of abolishing the FDIC argue that it would reduce government bureaucracy, but this approach disregards the essential role the agency plays in ensuring stability and trust in the financial system. While reducing inefficiencies in government is an admirable goal, it should not come at the expense of institutions that have proven indispensable in times of economic crisis. It’s a lot like a skydiving outfit deciding that to cut costs they are going to do away with parachutes. Not really bright.

Instead of considering drastic measures that put financial security at risk, policymakers should focus on strengthening the FDIC to meet modern challenges. Its role is as critical today as it was during its creation, serving as a cornerstone of trust and stability in the U.S. banking system. Removing it would not only be reckless but a step backward in safeguarding the nation’s economic well-being.