In today’s turbulent housing market, both homeowners and renters are grappling with a severe affordability crisis. Skyrocketing home prices and climbing interest rates have sidelined millions of potential buyers, while rising taxes and insurance costs further burden those who already own homes. For renters, the situation is equally dire, with rent burdens reaching unprecedented heights as rental costs soar.

Despite a surge in the construction of single-family homes and a wave of new multifamily rental units, the relief in affordability is expected to be modest. Strong household growth, persistent development constraints, and steep construction costs continue to thwart significant progress. This housing crisis is a complex web, demanding collective action from all stakeholders to address not only affordability but also related pressing issues like the inadequate housing safety net, the escalating number of people experiencing homelessness, and the looming threat of climate change.

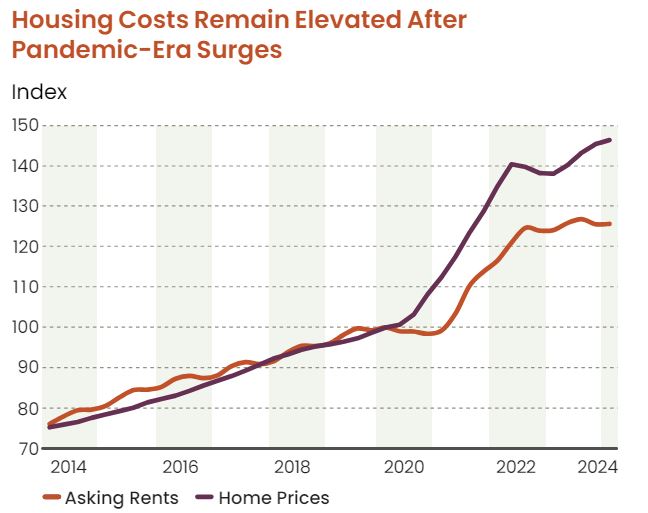

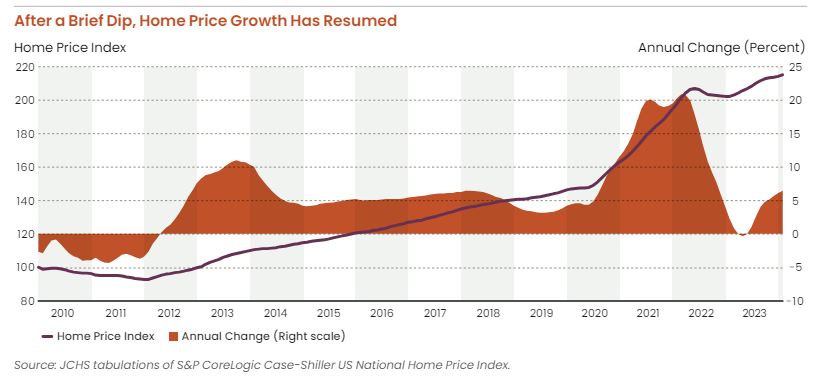

As of early 2024, the U.S. housing market paints a grim picture. Home prices have hit a new record high, driven by a remarkable 47 percent surge since early 2020, according to the S&P CoreLogic Case-Shiller US National Home Price Index. Even a brief dip in 2023 couldn’t stem the tide, with prices climbing 6.4 percent annually in February 2024 alone. The result? The median payment on home mortgage applications has surged, pushing affordability further out of reach for many Americans. For first-time buyers relying on low-downpayment loans, the total monthly cost for a median-priced home has ballooned to $3,096 after taxes and insurance, according to the Mortgage Bankers Association.

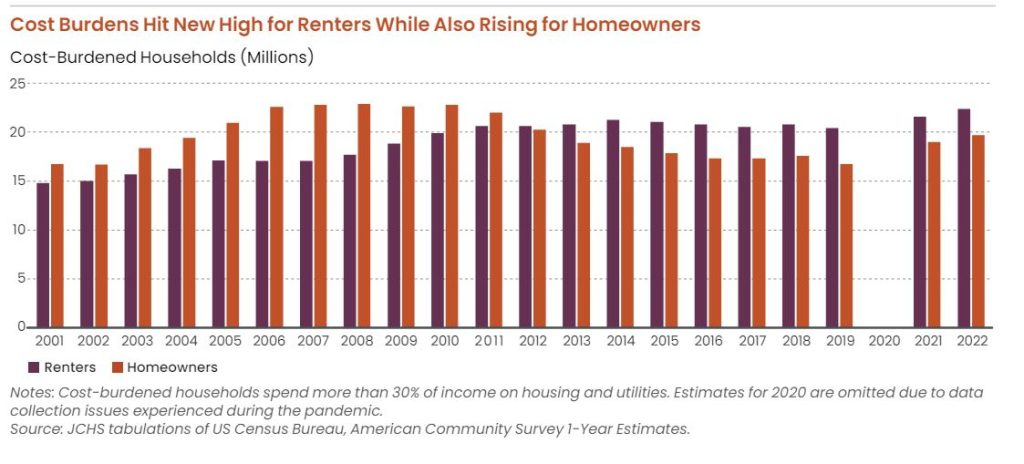

The affordability squeeze is painfully evident among homeowners. The number of households spending more than 30 percent of their income on housing and utilities – known as cost-burdened homeowners – soared by 3 million to 19.7 million between 2019 and 2022. Alarmingly, nearly a quarter of homeowner households now find themselves stretched dangerously thin, with older homeowners particularly hard-hit. For renters, the story is equally grim. Despite a cooling rental market as new units flood in, rent burdens have reached an all-time high, squeezing many households beyond their limits.

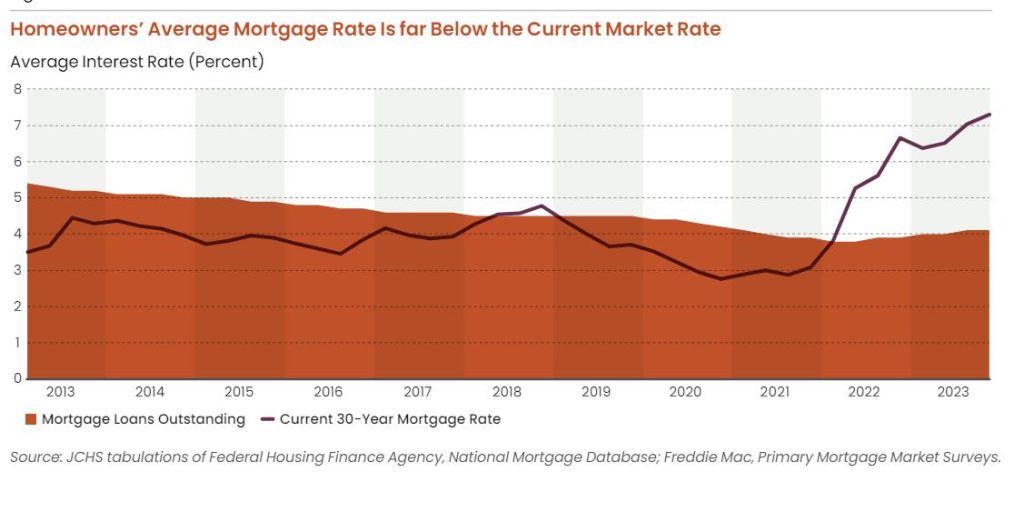

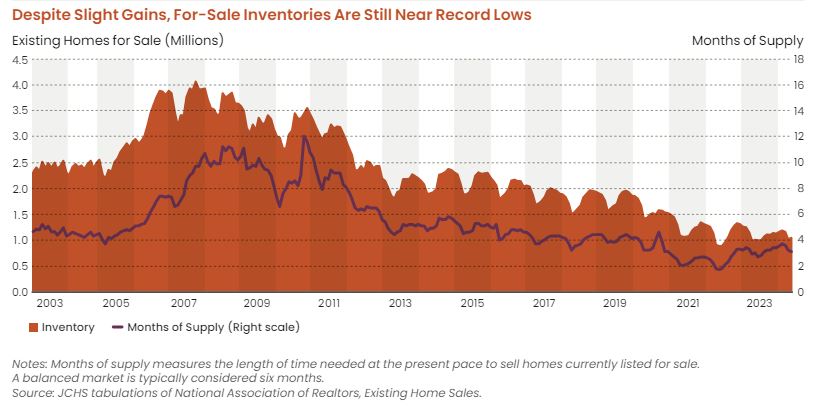

Compounding the issue, the supply of homes for sale remains critically low, largely due to the “lock-in” effect. Current homeowners with favorable mortgage rates are reluctant to sell and move, given that the average interest rate on existing mortgages is just over 4 percent compared to the current 30-year rate hovering around 7 percent. This disparity has slashed inventory levels, with only 1.11 million homes available for purchase in March 2024, a 34 percent drop from March 2019, according to the National Association of Realtors (NAR). The resulting scarcity has driven a significant reduction in existing home sales, with only 4.1 million homes sold in 2023.

Single-family homebuilding has been a beacon of activity amid the crisis, with construction steadily rising throughout 2023 despite high-interest rates. The pace of new builds has maintained a strong momentum into 2024, suggesting some relief may be on the horizon. However, the robust pace of construction is tempered by the realities of high costs and limited land availability, which continue to impede substantial gains in housing supply.

The rental market is experiencing its own transformation. Multifamily completions soared by 22 percent in 2023, the highest annual level in over three decades. As these new units have hit the market, the rental sector has cooled, with asking rents in professionally managed apartments rising just 0.2 percent year-over-year in the first quarter of 2024. This marks a sharp deceleration from the record-high increases seen in previous years.

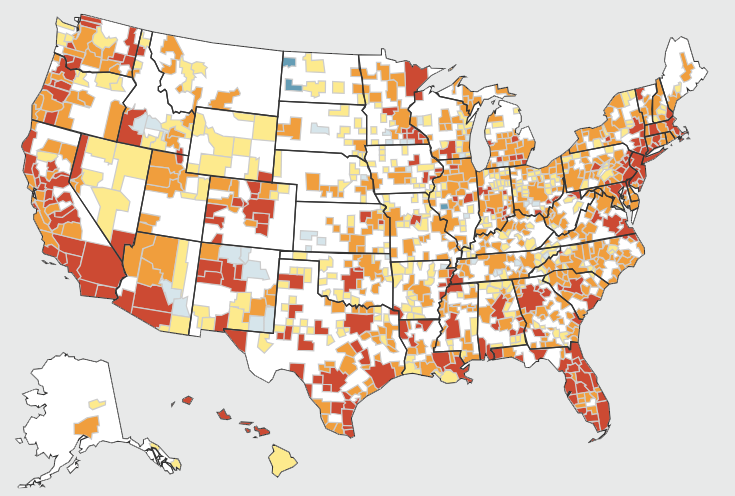

The situation is further complicated by broader demographic shifts. The pandemic accelerated a trend of migration from urban cores to suburbs and smaller metropolitan areas. This pattern, bolstered by a swell in immigration levels in 2022 and 2023, has significantly boosted population growth and reshaped housing demand across the country.

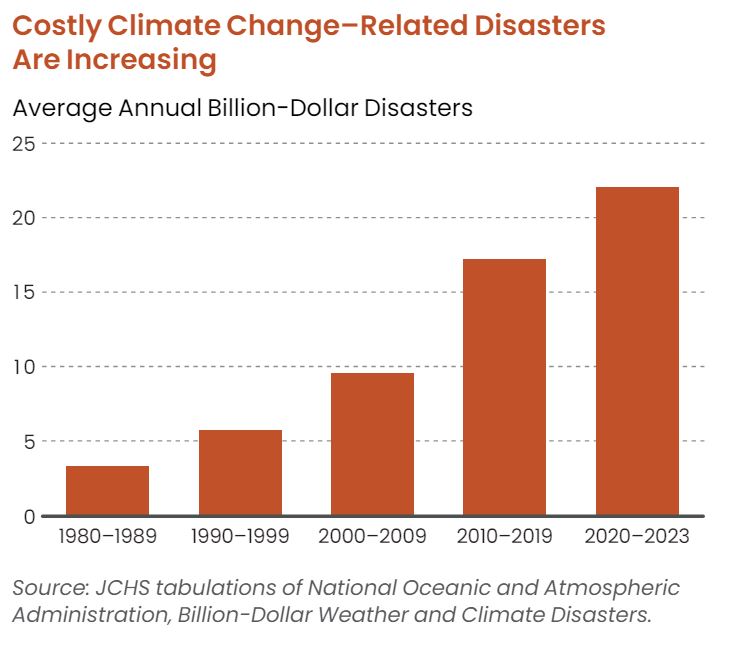

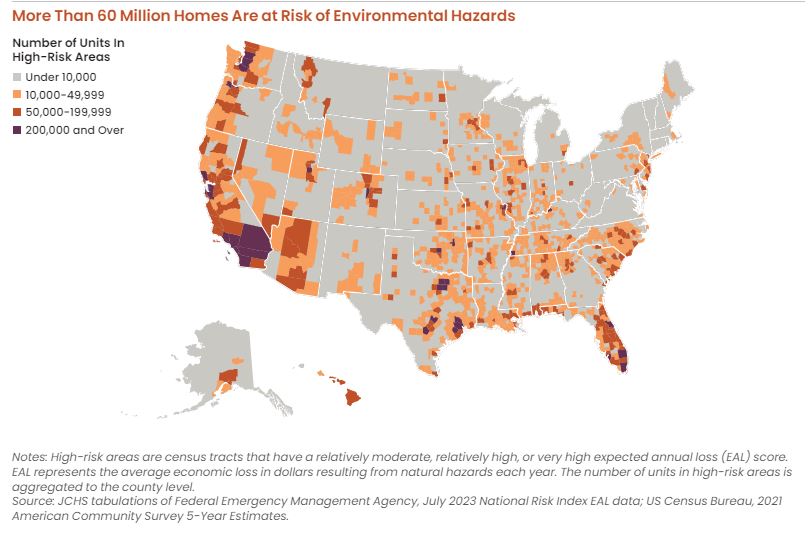

Adding to the pressures are the escalating risks posed by climate change. The frequency of billion-dollar disasters has exploded from an average of three annually in the 1980s to a staggering 28 in 2023. As extreme weather events become more common, the vulnerability of the housing stock to severe damage continues to rise, exacerbating the already precarious situation for homeowners and renters alike.

The housing market’s current trajectory underscores the urgent need for comprehensive solutions. Policymakers, developers, and community leaders must collaborate to tackle the myriad challenges of affordability, supply shortages, and climate resilience. As the storm clouds of this crisis gather, the call to action is clear: it’s time to address the housing crisis with the urgency and innovation it demands.