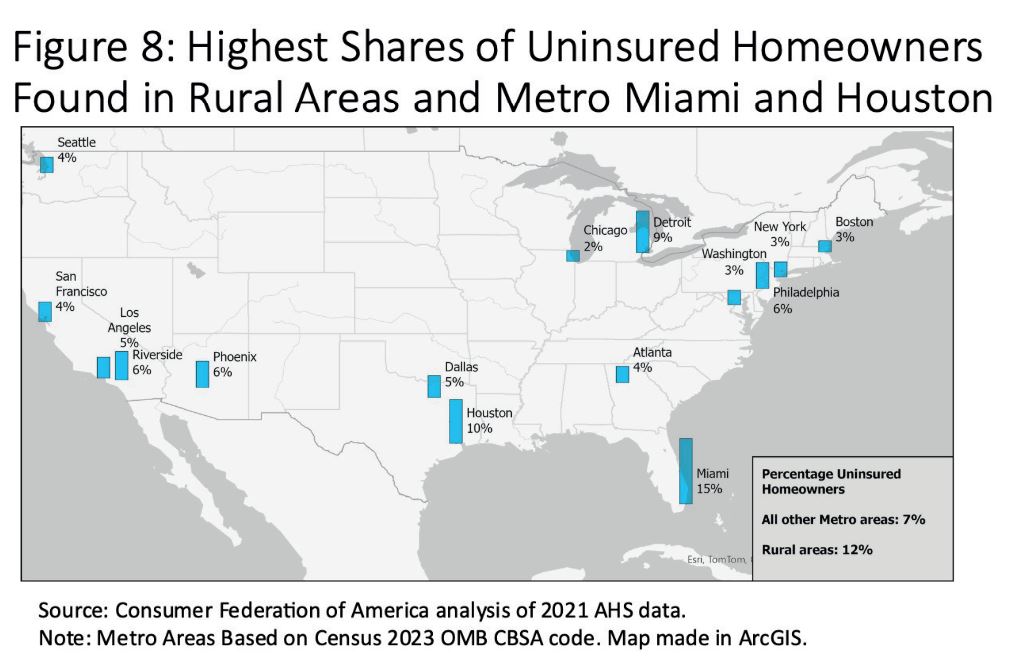

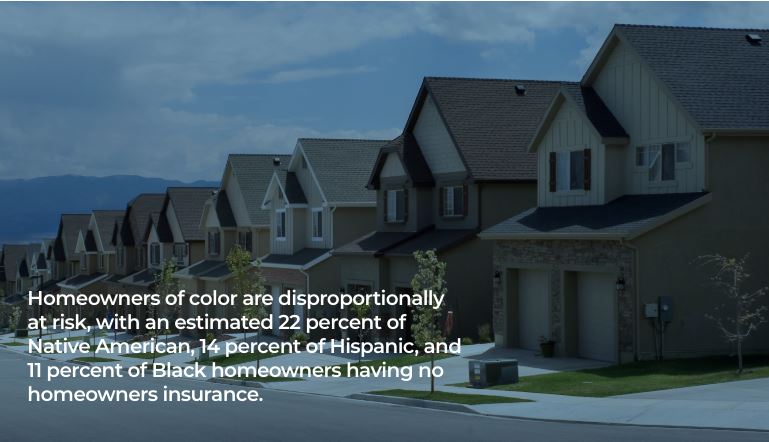

In the sunshine states of Florida and Texas, a silent catastrophe brews, hidden in plain sight: According to a report released by the CFA, over 10% of residential homes remain uninsured, leaving communities vulnerable to the devastating impacts of natural disasters. With hurricane season looming, the specter of a Category 5 hurricane threatens to unleash a wave of destruction with far-reaching consequences, overshadowing the already staggering number of homeless individuals across the nation.

The potential aftermath of such a catastrophic event is dire, with consequences rippling far beyond the immediate physical damage. One of the most alarming prospects is the exponential increase in homelessness. With no insurance to rebuild their homes families could find themselves displaced, the number of individuals without home insurance is 4 million between Texas and Florida alone—an alarming figure when compared to the existing total of approximately 580,000 homeless individuals across the entire United States.

As the ranks of the homeless swell, so too does the risk of an uptick in crime. Desperation often breeds criminal activity, and the newly homeless may resort to illegal means to survive, further destabilizing already fragile communities.

The economic fallout from uninsured homes cannot be overstated. Property values are poised to plummet in the wake of widespread destruction, eroding the wealth and equity of homeowners across the region. With decreased property values comes a corresponding decline in property tax revenues, placing additional strain on local governments already grappling with the costs of disaster recovery.

Compounding these challenges is the exodus of residents and businesses fleeing the escalating cost of insurance. Climate change has driven up insurance premiums to untenable levels, pricing out many homeowners who can no longer afford coverage. As a result, communities face the prospect of hollowing out, as both individuals and businesses seek refuge in more financially viable locales.

At the heart of this crisis lies the undeniable reality of climate change. Rising temperatures and increasingly volatile weather patterns have made hurricanes more frequent and destructive, rendering traditional insurance models obsolete.

As insurers pass on the mounting costs of climate-related disasters to homeowners, the cycle of unaffordability perpetuates itself, trapping vulnerable communities in a downward spiral of risk and economic hardship.

Addressing the root causes of the uninsured homes crisis requires a multifaceted approach. Investing in resilient infrastructure, implementing stringent building codes, and expanding access to affordable insurance are essential steps in mitigating the impacts of future disasters. Proactive measures such as community outreach and education can help empower homeowners to safeguard their properties against the ravages of climate change.

In the face of mounting challenges, the time for action is now. Florida and Texas stand on the precipice of a catastrophe of unprecedented proportions, one that threatens to reshape the social, economic, and environmental landscape for generations to come.

Only by confronting the underlying factors driving the uninsured homes crisis can we hope to build a more resilient future for all who call these vulnerable regions home.